After not being super thrilled about how an issue was handled this past summer, ended up not needing the claim, ive been looking into changing carriers. In full disclosure, its my fault for not knowing the ins and outs and asking right questions.

Have spoken with a local Erie agent and price wise it will be a little more than im currently paying, but with all the CCC talk and this and that when i brought it up he said i wouldnt need it cause i wouldnt be under the care, custody, or control of anyones property… i disagree with him there as we are there to take care of cleaning someones property and accidents do happen.

But below is what he sent back. Just wanted to get some thoughts and opinions. I have spoke with my current carrier and they can add CCC and up coverage amount from where i currently am.

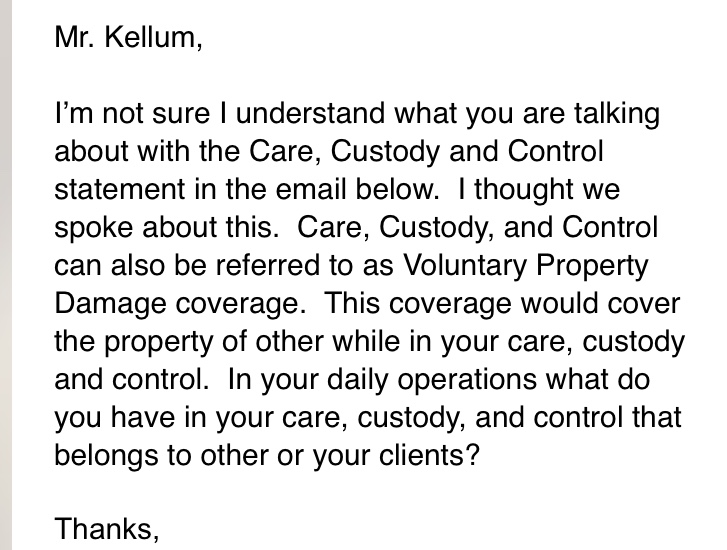

It my understanding you dont need care and custudy since you are not using/handling the clients possessions.

It is under gl.

Verifly seems legit.

I am switching at the end of the month to travelers.

If you are in NC pm, ill get the agent info when i get home, she us from Raleigh

If you spray the wrong chem on the side of a house and it discolors it, GL isn’t going to cover it. That, and other scenarios are why you need to be fully insured, including CCC.

what you say makes sense, I gave that scenario to my agent, and she told me that I did not need CCC for it.

That was covered by GL.

I even asked about over spraying, lets say a car got sprinkled with SH, and she said it was covered under GL, regardless of wheather it was a clients car or the neighbor.

she gave me an explanation on CCC… if I were to move the car for the client or if the client left me the keys to move it then I would need CCC.

I do residential cleaning so CCC was on my mind, since we are usually “in charge” of the home while we clean, but she tells me that it is covered under GL.

I’ve come across the CCC discussion on here enough times to interest me enough to do a little research. Nearly everything I’ve read says you have to be able to posses the property and the exclusion does not apply to real property such as a building.

" Property Damage Exclusion

Among the property damage exclusions in the post-1988 edition Insurance Services Office, Inc. (ISO) commercial general liability (CGL) policy is exclusion j.4.—excluded from coverage is any property damage to personal property that is in the care, custody, or control of the insured.

We sometimes forget how easy it is to assume everyone knows our insurance lingo. I was reminded of this a while back when a client remarked “it’s not personal property—the business owns it.” So it is worth pointing out that, in the context of this exclusion, the reference is not to ownership (business or personal), but rather the type of property. In other words, the exclusion does not apply to property that is considered real property, such as a building"

If this is not true I’d like to see it, because everything I’ve read says real property is not part of the exclusion. I’ve brought it up to a couple different agents when looking for insurance and they look at me like I don’t know what Im talking about. Maybe CCC is something to worry about as far as real property is concerned, but I can’t find anything about it. I only find just the opposite.

I’ve read all the examples but unfortunately none have anything to do with real property. Which always takes me back to the beginning of the article that says real property is not part of the exclusion. Also , there is a possession factor, It’s impossible to posses someone’s home while your washing it.

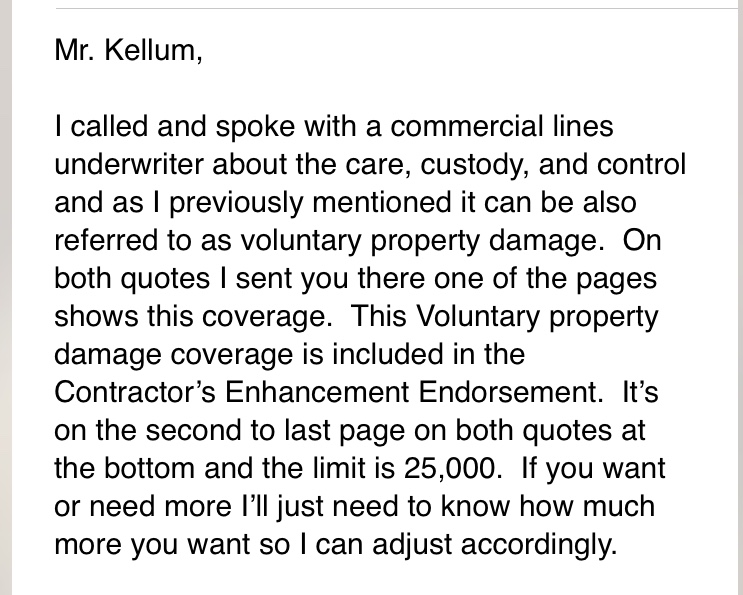

I did some searching, and found the same thing, CCC doesn’t cover the house/property. If you break someones window ccc will not cover that, because you where not hired to mess with any windows. CCC only covers you for what you where hired to do. From what im reading you need a voluntary property damage plan to cover the house/property.

I appreciate the article. I can see that having some real property coverage in addition to your GL policy would be beneficial. The article goes on to say that that coverage amounts to a couple hundred bucks a year. Which it should be since 20 to 25 grand in coverage would be adequate for 99 percent of peopl’s siding, driveways, sidewalks, decks, etc., and that’s a small hit to an insurance company. CCC is an exclusion that applies to personal property, not real property, but to be fully covered maybe you do need a real property enhancement.

I just switched to liberty.

Also spoke to NationWide before transfering.

I went over what that link reffers as CCC.

As many know i own a residential cleaning, and i have been told again i do not need CCC, that if the examples described happen i am covered under GL

If i were in the moving business, transportation, or restoration, where i hold or haul or restore them while i conduct my business then yes i need CCC.

Now painters, or general contractors might need them depending on the services they provide.

Thanks. Will do. There’s a lot of tiles and shingle roofs down here. Of course a lot of concrete as well. When investigating insurance though nobody wants to touch S. Florida Lol. So I think I will eventually have to figure that one out (maybe combine it with another service).

Frank Crum is based out of Florida and will insure walking roofs to soft wash them. I’d check with them. Www.frankcrum.com also see if anyone else from Florida has recommended things here.

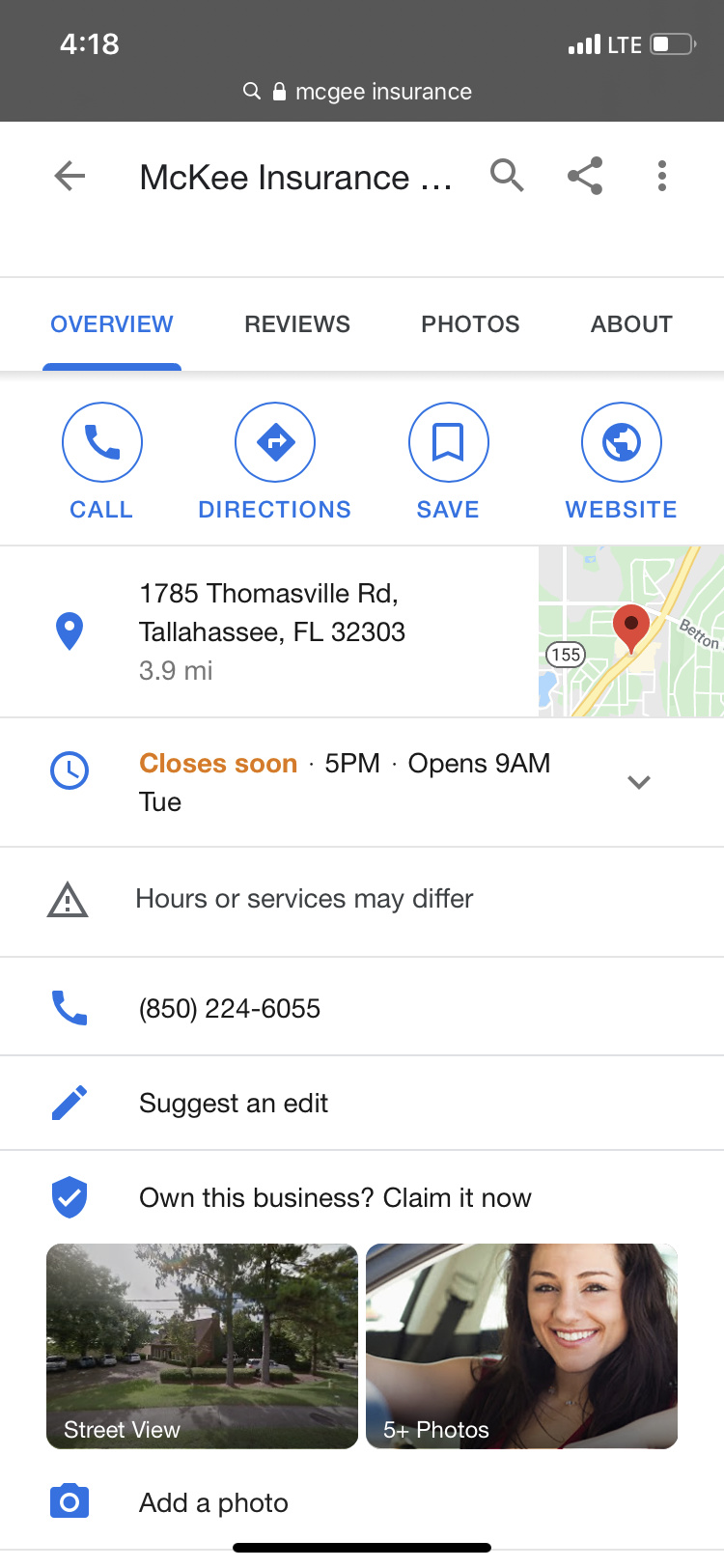

Know I’m a bit late but Patrick with McKee insurance agency has me and a couple other guys on here insured. $438/ year for roof walks and a 1 mil liability. I suggest giving him a call

If you look on their website they list their insurance carriers. Nationwide, Auto Owners, etc, etc, etc. I believe McKee is just the agent. A lot of agencies call themselves “so and so” insurance. Do you know which carrier you’re insured through? I’m just curious because the price is so cheap. I’d like to see if it’s a provider I can get in my state. I wonder if you get lower rates in FL because of all the pressure washing companies though.