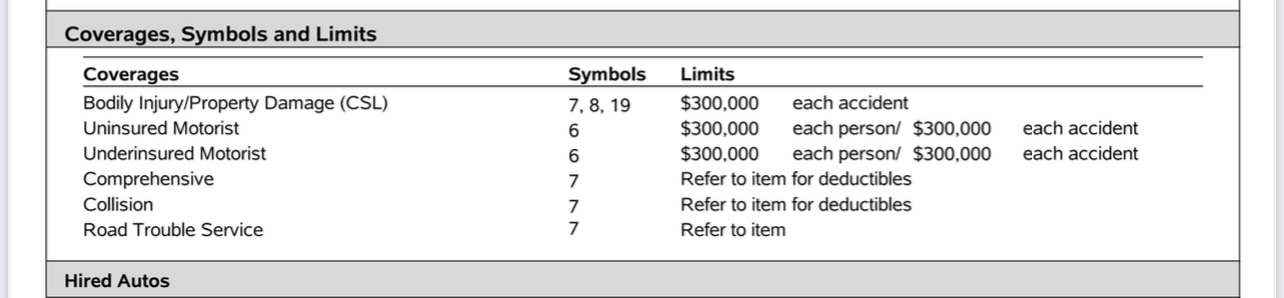

Okay guys, I received a quote from my agent for commercial auto for truck and trailer. But I saw $1,000,000 limits and I can’t see how I need that for auto. Yes for business GL but for my vehicle? So my agent sent these 3 limits. Which one would be a better decision? 300, 500, or 1 M?

Do I need it that high for auto when I already have million GL for the business? Don’t want to pay for something I won’t need.

I’m solo right now, but I’ll be hiring soon so I’ll need commercial auto. Curious to the amount you were quoted cost wise?

I’ve seen 1 million more than once from commercial clients, so if you do commercial you may need it. Also, I’ve gotten by on my personal auto, which may not have been advisable but they just had me raise it to 100k and then they were fine.

I’m a million, usually not a whole lot more. If you are a business and get into an accident, people love to sue companies, they figure your loaded and are good for it, so…wouldn’t go less than 500,000 for sure. That’s just my opinion.

My main concern is not getting work from it I have million dollar general liability for commercial work but do I require it on my auto as well in order to do commercial work. I don’t think I do but I’m not sure. The cost difference on the policy between 300,000 and 1 million is crazy. I save so much more going lower and 300k to me still seems like a lot!

It depends on commercial work, some ask for minimums before you can bid, so…if doing mostly residential you will be fine as far as that goes. But if your truck has signage and trailer hooked to it, I’d go as high as you can afford. You get into an accident and hurt someone, they will get attorney’s and go after you. Your million dollar GL won’t cover that on the street. So weigh it out…

I know commercial companies ask to to see your 1M GL policy for the business, have they asked to see your auto policy as well?

The million sounds like the standard, I’m just curious if it affects any work you get. Talking about auto not the business insurance. My GL is already 1M

They have for us in the past, they like to see million across the board for GL and Auto. It just depends on the management or company’s requirements. You could go lower and if told you need higher to bid or get a job, deal with it then…

Yeah, mine is truck, trailer, tools and equipment covered. I cheap out and raise my deductible. I will never call them for anything less than a grand to a grand and a half anyway. Not worth the increase in premiums.

I don’t think $1m for commercial liability coverage is all that crazy. If the worst were to happen, say you hit someone and they became paralyzed, they will likely require professional care for the rest of their lives. That adds up.

@DJPWS In my experience the PM sends me a sample COI and I either meet that and can work for them or not. Sometimes if their requirements are high (like above 2 million for GL) I ask if they would make an exception based on what I’m doing, or if it’s a really big project I’ll either bite the bullet or add it to the quote. (I haven’t had one big enough yet for either) I have 2 million GL, and that makes most happy. For the sample COIs I’ve seen, 500k-1 mil is the most common. Workmans comp usually runs around 500k but I’ve seen 1 million a some times.

I do a bunch of commercial and I’ve never had anyone ask about vehicle insurance. I’d go with the smaller limits. You’re not GM. You’re a guy with a pickup and a small trailer. No lawyer going to spend much time against you for more than readily available insurance.

On another note, you may want to keep most your non-business valuables in your wife’s name. At one point in my career I was a pretty large developer and often had my name on many millions worth of loans. In fact my goal in those days was to get to $150myn because back then, that was kind of the ‘too big to fail’ number, lol. So I just got in the habit of never showing any non-business assets.

My .02 on insurance is this, no matter what your coverage is, if you get a shyster shark on you you are done. They will find a way to pierce the veil of your LLC and get you unless you hire your own shark to teach you how to hide things correctly. Even then, a shyster will use an investigator to find where you slip up at so that they can take that to court, or smear you so you look like a turd in court for an easy payday. That is the game and that is how it is played. Do like racer says, hide your assets,. Maybe change your name, go deeep deeeeeep undercover by wearing a ball cap and big, bright orange rimmed glasses, oh wait that is heath. LOL.

If you live in a state where they don’t award punitive damages you are much better off. Way harder to get the mega million payday that way.